")

{kind=link}

Carol Johnson, Southern Indiana Business Report

Interest rates are the highest since 2014 as the Federal Reserve has raised rates to slow spending and control inflation.

With rates now over 6%, the once red-hot housing market has cooled somewhat. There are still buyers hunting for homes, but the number of homeowners rushing to refinance at a lower rate has dissipated.

If you’re a saver, however, the bump in interest rates is good news. Banks are beginning to offer better rates on savings products such as Money Market accounts and certificates of deposit (CDs).

Cole Watson is senior vice president and controller for Hoosier Hills Credit Union. With any sudden change in rates, there are winners and losers, he said.

“Starting in March of 2020 to March of 2022, if you walk it back, the Fed did a series of emergency moves when COVID hit and it triggered a refinance boom. You saw demand for homes skyrocket and that boosted home prices through the first quarter of this year,” Watson said.

Low mortgage lending rates created a huge surge in demand and housing inventory couldn’t keep up with that demand, which pushed up home prices. Interest rates have doubled since the start of 2022 and those who are now ready to buy a home may be rethinking how much home they can afford.

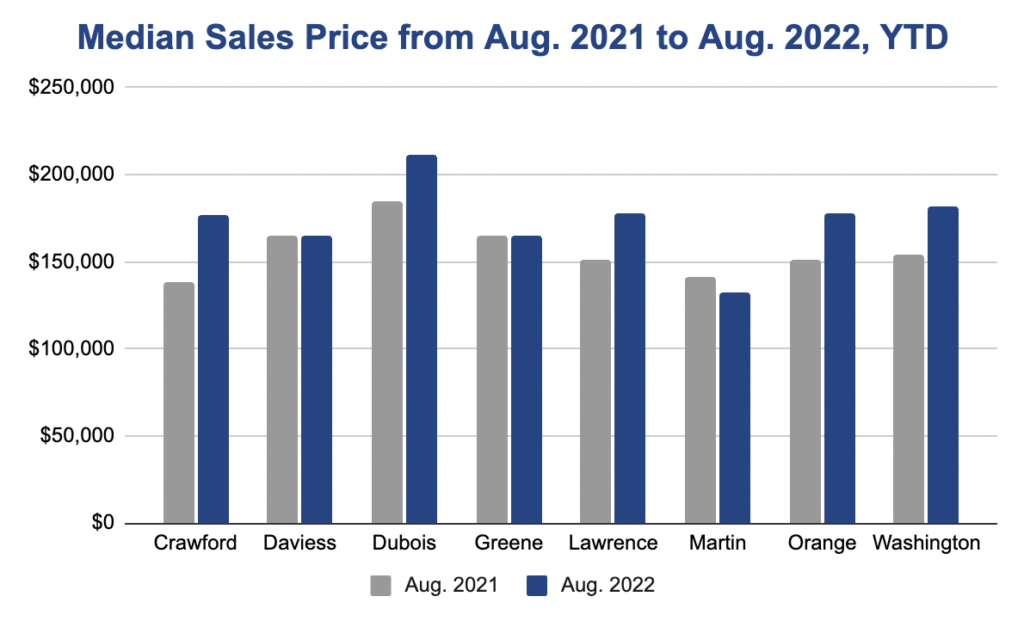

According to the Indiana Association of Realtors, Indiana’s housing market continued to cool in July, as sales of existing homes (8,614 for the month) finished 10.3% below July 2021. This puts year-to-date sales nearly 4% below the first seven months of 2021.

In positive news for homebuyers in the market, Indiana’s median sale price dipped to $246,000 in July from $250,000 in June. Median prices through July are trending 14% higher year-to-date, but only 10% above July ’21 as year-over-year price appreciation slows.

Good news for savers

Watson said there is an upside to the changing rates. If you’re a saver, however, the bump in interest rates is good news. Banks are beginning to offer better rates on savings products such as Money Market accounts and certificates of deposit (CDs).

“Savers are the beneficiary of this higher rate environment,” he said.

Watson said financial institutions are beginning to offer more aggressive rates and consumers who want to take advantage of those offers should look into what incentives are available.

“We just launched a 22-month CD (with a) 3.04 APY and we continue to look at ways to offer the best rate we can,” Watson said.

You have to go back 40 years to the last time banks and credit unions offered high yield interest rates on deposits. In the 1980s, consumers saw double-digit CD rates, but mortgage rates were also in the double digits.

Watson said financial institutions will need to get the message out to younger people that their money can work for them.

“Baby boomers, they remember when you could earn a solid interest rate on a timed deposit. For younger generations, they have literally lived as an adult where there were no meaningful deposit rates. It’s incumbent on us to educate them,” Watson said.

Back to the housing market, Watson urged buyers to look beyond interest rates when searching for a home they can afford.

Increasing home values translate into an increase in assessed value and property taxes. Buyers should make sure they are aware of those additional costs of home ownership.

Although interest rates aren’t as enticing as they were, Indiana Association of Realtors CEO Mark Fisher said housing remains a sound investment.

“Home prices are settling towards a more sustainable pace, but still gained over 14% this year while the national economy shifted into reverse,” Fisher added. “For Hoosier homeowners and sellers, that’s a sign that housing remains a great wealth-building investment and a valuable commodity even as we enter a more balanced market.”